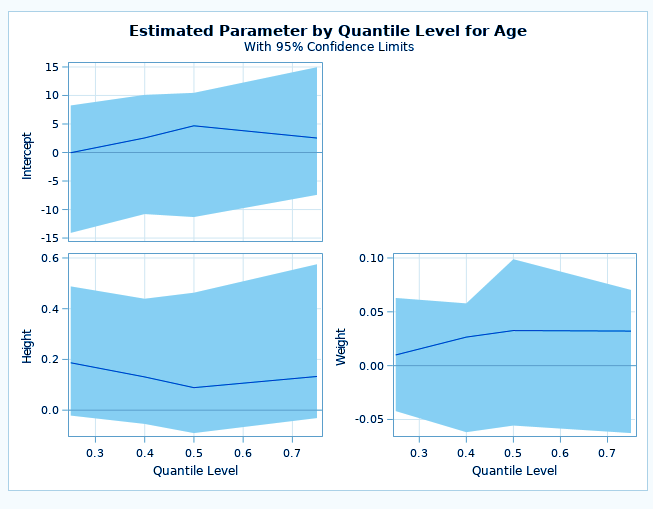

Bayesian Quantile Regression Sas. Node 25 of 0. Estimation of the regression quantiles is based on a likelihood-based approach using the asymmetric Laplace density.

Ordinary least squares regression models the relationship between one or more covariates X and the conditional mean of the response variable Y given Xx. The QUANTSELECT procedure computes the Bofinger bandwidth. Mar 16 2012 We propose quantile regression QR in the Bayesian framework for a class of nonlinear mixed effects models with a known parametric model form for longitudinal data.

Inference about the posterior distribution of the parameters of this regression function is made by means of a Markov chain Monte Carlo MCMC algorithm.

Quantile Regression Tree level 1. Based on the Bayesian adaptive Lasso quantile regression Alhamzawi et al 2012 we propose the iterative adaptive Lasso quantile regression which is an extension to the Expectation Conditional Maximization ECM algorithm Sun et al 2010. Compute quantile-level bandwidth. SAS provides convenient tools for applying these methods including built-in capabilities in the GENMOD FMM LIFEREG and PHREG procedures called the built-in Bayesian procedures and a general Bayesian modeling tool in the MCMC procedure.