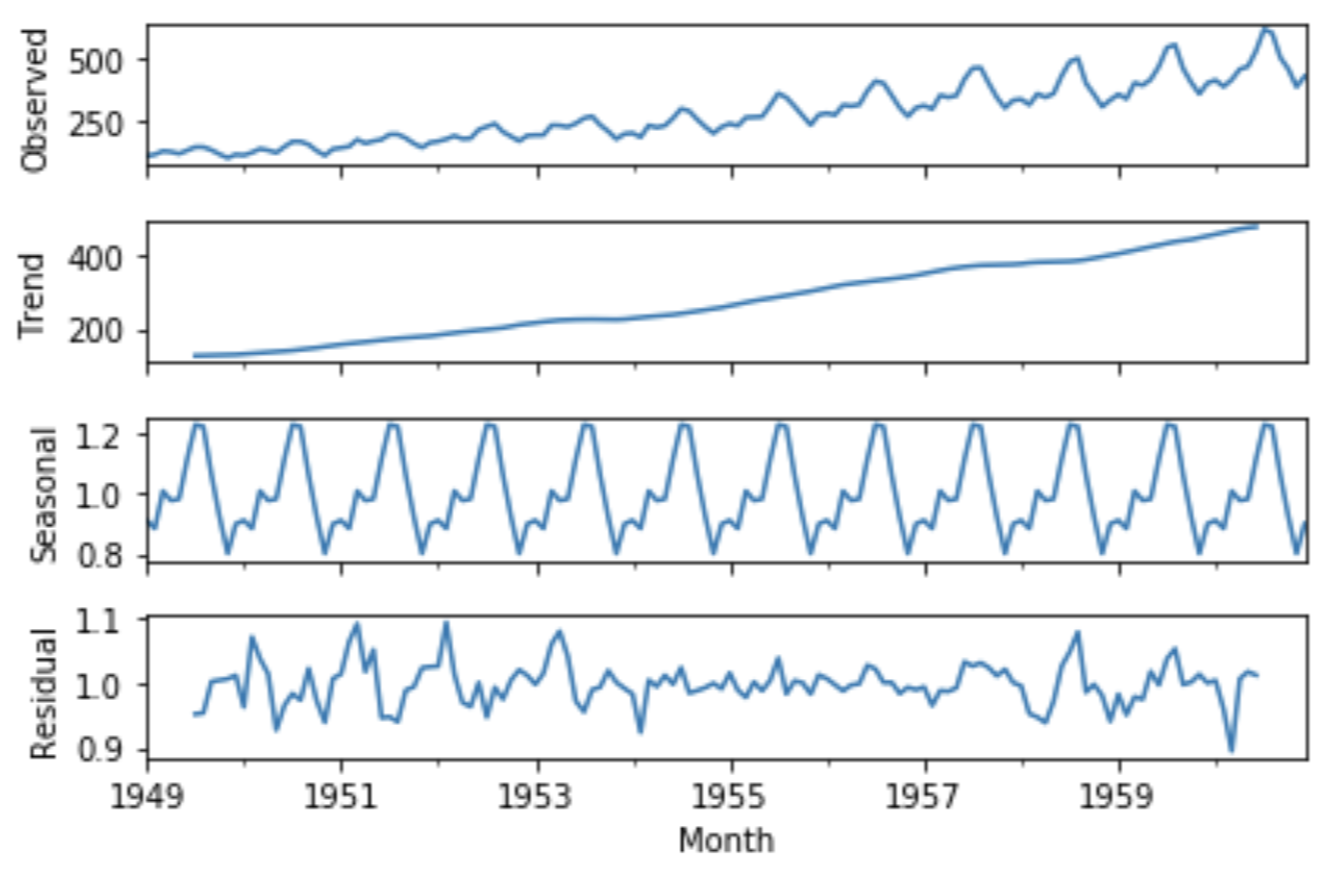

Arima Regression Seasonality. A seasonal ARIMA model is formed by including additional seasonal terms in the ARIMA models we have seen so far. We use uppercase notation for the seasonal parts of the model and lowercase notation for the non-seasonal parts of the model.

Aug 21 2019 Seasonal Autoregressive Integrated Moving Average SARIMA or Seasonal ARIMA is an extension of ARIMA that explicitly supports univariate time series data with a seasonal component. It adds three new hyperparameters to specify the autoregression AR differencing I and moving average MA for the seasonal component of the series as well as an additional parameter for the period of the seasonality. This is essentially aseasonal exponential smoothing.

Sep 07 2020 SARIMA is seasonal ARIMA and it is used with predict time series with seasonality.

It also allows all specialized cases including. - Connects to forecastArima. Seasonal ARIMA models Weve previously studied three methods for modeling seasonality. If appropriate we fit regression effects along with the ARIMA models to estimate trading day andor moving holiday effects and the software removes these effects from the series before estimation of the pure seasonal trend-cycle and irregular components.